Why Fast Suicide Cleanup Is Critical: Time, Odor & Health Risks

August 19, 2025

The Legal Requirements for Suicide Scene Cleanup by State

October 20, 2025

When tragedy strikes and a suicide occurs on a property, one of the least expected but most urgent questions is: who pays for the cleanup? Families and property owners often find themselves unprepared for the financial burden of biohazard remediation. In this guide, we break down suicide cleanup cost, how insurance typically handles it, and what steps you can take to manage costs and claims.

Understanding Suicide Cleanup Cost

“Suicide cleanup cost” is a term that tends to shock many, because the ranges are wide and the factors numerous. A few key benchmarks and cost drivers:

- On average, biohazard/death scene cleanup ranges from $1,500 to $5,000 for moderate jobs, though more extensive cases can go well beyond that.

- For high-complexity scenes (multiple rooms, structural damage, odor remediation), total costs of $10,000 to $25,000 are not uncommon.

- In some cases hourly rates can be in the $200–$300 per hour range (or higher for extreme hazard levels) depending on location, risk, and complexity.

Costs depend heavily on:

- Extent of contamination – how many rooms, whether bodily fluids have seeped into flooring, walls, subfloors, or adjoining rooms.

- Time until discovery – longer unattended periods often mean more decomposition, odor, and deeper contamination, requiring more intensive remediation.

- Method of suicide – firearm incidents often have wider splatter zones, affecting ceilings, walls, and adjoining areas.

- Structural damage or odor remediation – if parts of the structure (drywall, carpeting, subfloors) must be removed or replaced, or if industrial odor-neutralizing equipment is needed.

- Regulation, disposal, and location – disposal of biohazard waste, travel fees, regulatory compliance, and local cost of labor.

Because of these variables, cleanup companies usually conduct an assessment or site visit before issuing a final estimate.

Who Typically Pays for Cleanup After Suicide?

There are several possible responsible parties — the key is to understand how to tap into coverage or negotiate responsibility.

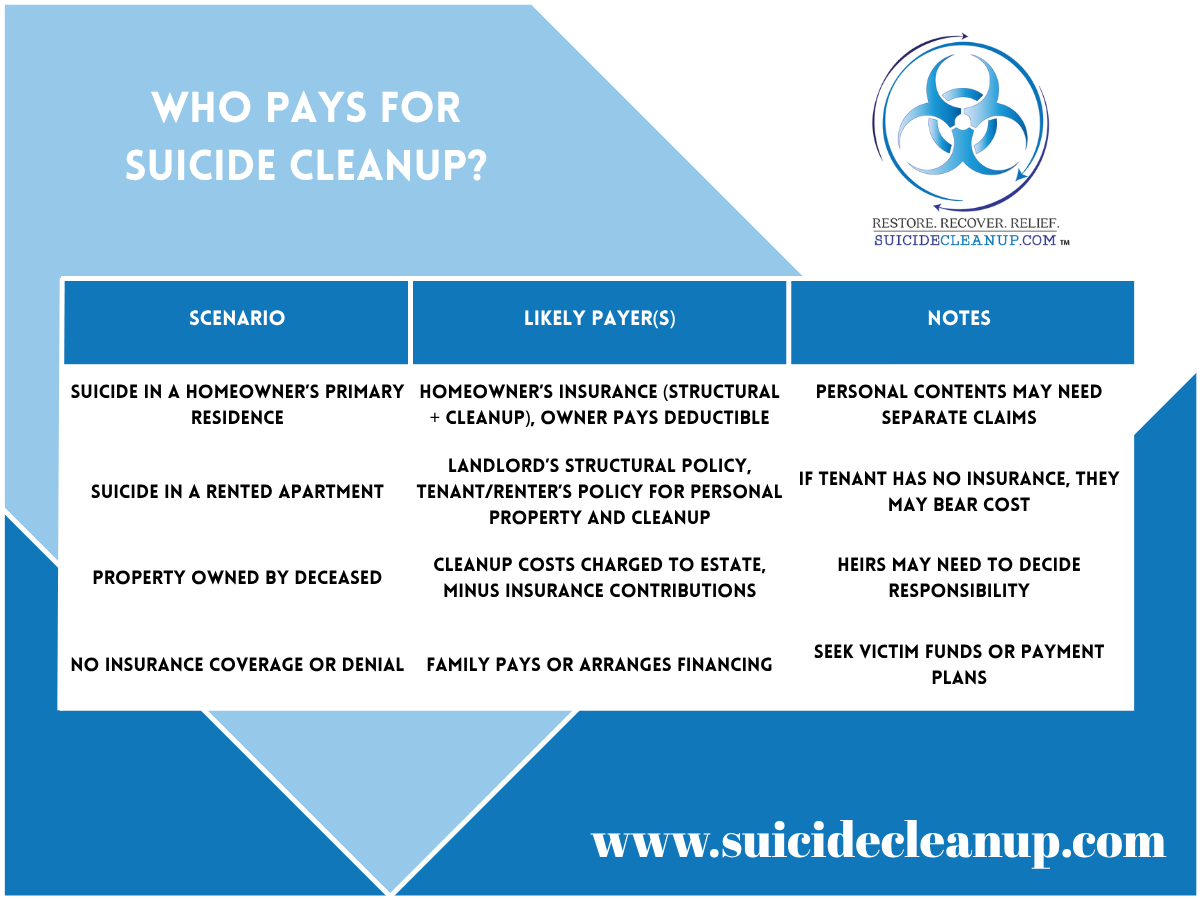

1. Homeowners Insurance / Property Owner Insurance

In many cases, homeowners’ insurance policies cover biohazard or death-cleanup services, as they treat most death cleanup under “all-risk” or property damage coverage.

Important caveats:

- The insurance company often requires that a licensed, certified biohazard cleanup provider do the work (versus ad-hoc or volunteer cleanup).

- Deductibles apply; often the homeowner must pay up to their deductible before insurance kicks in.

- Some policies may have limits or exclusions for personal property (e.g. furniture, carpeting) or might not fully cover odor remediation or structural replacement.

- The insurer may require documentation (photographs, invoices, proof of method) to process claims.

- Insurance companies are not allowed to “steer” you to a specific cleanup firm (that would be a conflict of interest). You can choose your own provider.

If you are a property owner or landlord, your policy may cover structural remediation (walls, floors) but may not cover tenant property or personal belongings. In that case, the tenant or their insurance (if any) could be responsible for contents.

2. Renter / Tenant Responsibility

If the property where the suicide occurred is leased:

- The tenant (or estate of tenant) is often financially responsible for damage to their own contents (furniture, carpeting, personal items).

- A renter’s insurance policy may cover part or all of the necessary cleanup, depending on the policy’s coverage of “additional living expenses,” “liability,” or specialized biohazard add-ons.

- If the landlord’s insurance picks up structural cleanup, they may seek to recoup costs from the tenant or their insurer if leases allow.

3. Estate of the Deceased / Heirs

In situations where the deceased owned or controlled the property, their estate may be legally liable for cleanup costs. Heirs or executors may need to allocate funds accordingly.

4. Out-of-Pocket / Financing Options

When insurance is unavailable, denied, insufficient, or there is no applicable coverage:

- Families or property owners may need to pay out-of-pocket.

- Many biohazard cleanup companies offer financing plans, installment payments, or emergency payment assistance.

- In some jurisdictions, crime victim compensation funds can assist with trauma or biohazard cleanup costs under the Victims of Crime Act (VOCA) or similar state programs. These funds often have eligibility criteria and require application.

Insurance & Claim Strategies: What Families Should Know

To improve your chances of coverage and minimize out-of-pocket burden, follow these best practices:

- Review your policy carefully

Before a crisis, check whether your homeowners or renters policy includes “biohazard,” “trauma scene cleanup,” or “death cleanup” coverage, and note the limits and exclusions. - Use a licensed cleanup provider

Select a firm experienced in suicide cleanup or trauma remediation. Many of these companies are comfortable working directly with insurers and can help handle the claims paperwork. - Document everything

Take detailed photographs, keep all invoices and quotes, track communications with your insurer—these materials are essential when filing a claim. - File promptly

Report the incident and begin claims as soon as possible. Delayed cleanup can worsen contamination and increase cost, which insurers may question. - Negotiate and appeal denials

If an insurer denies coverage, ask for specific policy language, appeal the decision, or enlist help from a public adjuster or attorney. - Ask cleanup company for help on claims

Many trauma cleanup firms can work directly with the insurer, submitting documentation on your behalf, or providing standardized reports to support your claim. - Explore victim assistance / state funds

If insurance fails you, check local or state victim compensation programs that may cover cleanup of crime or trauma scenes (this varies by jurisdiction).

Example Scenarios: Who Pays?

Key Takeaways

- Suicide cleanup cost can range from a few thousand dollars for moderate cases to tens of thousands for complex or large-scale remediation.

- In many cases, insurance suicide cleanup coverage exists, especially under homeowners or commercial property policies, as long as cleanup is handled properly.

- The responsible party may be the homeowner, landlord, tenant, or the estate, depending on circumstances and lease/policy terms.

- To maximize coverage and minimize disputes, select a certified cleanup provider, document thoroughly, file claims promptly, and know your rights to choose your own remediation firm.

If you’re dealing with the aftermath of a suicide on a property, SuicideCleanup.com is here to help. We partner with licensed, insured biohazard teams that understand insurance and claims processes. Contact us for a free consultation and assistance navigating cleanup and coverage.